The Problem with Treasury Bonds is the Issuer, not the Economy

The robustness of this economic cycle continues to be stronger than most anticipated. GDP came in at 4.9% for Q3. If you look at headlines across the board, from inflation to wage growth to GDP, it may appear as if the economy is booming. Anticipating the turn in an economic cycle is just like watching paint dry. This market has been the story of the Super 7 stocks in the US (Apple, Microsoft, Alphabet, Meta, Tesla, Nvidia), coupled with the Semiconductors and GLP-1 companies.

Bonds Continue Their Decline

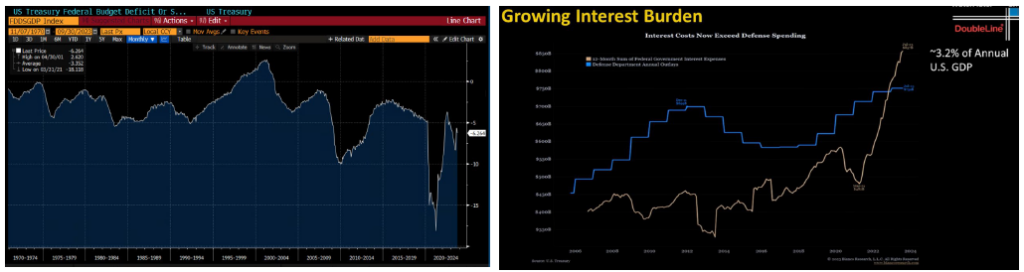

Bonds continued their decline, falling at a near record pace and extending their 3+ year drawdown, starting during Covid (the 30-year treasury bond peaked April 2020, while the 10-year peaked July 2020). The 30-year treasury bonds have lost 60% of their value since Covid, a drawdown that is even greater than the US stock market drawdown in 2008-2009. Higher for longer has finally hit the long end of the yield curve. The US Treasury Federal Deficit is currently at -6.26% of record level GDP numbers. To put the debt burden into perspective, the Government Interest Expense is expected to surpass Defense spending next year. That approximately 3.2% of annual GDP spending on interest expense is basically the equivalent of only paying your credit card minimums each month.

Credit spreads and defaults have picked up as of late. The numbers are still within the range of historical averages, but that could change soon. Some have questioned why duration is getting hit and corporate spreads have not widened. It is a difference of balance sheets and debt issuance maturity. The US government has a balance sheet problem. Eventually, this will also lead to much wider spreads across the risk spectrum, but it is hard to say when. Credit spreads have been suppressed as corporations were able to minimize overall issuance, which ultimately builds up a wall of issuance coming due in the next few years. Over the last few years of these commentaries, a theme of ours has been that sometimes the duration of economic stagnation, rather than the magnitude of a recession, is more telling of the longer lasting economic impacts it has. Eventually we will hit that maturity wall. Q4 of 2023 and all of 2024 will face the massive maturity wall of the government, while corporates are a little better spread out between 2024-2027.

Read the full commentary here.

Disclosure

All investments carry risks, and investors may lose their principal.

The material provided here is for informational purposes only and should not be considered personalized investment advice. The investment strategies mentioned here may not be suitable for everyone, and each investor should review their own situation before making an investment decision.

Opinions expressed here are subject to change without notice due to market conditions. Third-party data presented here is obtained from sources believed to be reliable, but accuracy, completeness, or reliability cannot be guaranteed.

The examples provided are for illustrative purposes only and should not be considered reflective of actual results.

Investments’ value and income can fluctuate, and investors may not recover their initial investment. Factors that can affect investments include interest rate changes, exchange rate fluctuations, general market conditions, political, social, and economic developments, and other variable factors. Investment carries risks, such as payment delays, and loss of income or capital. Neither Toroso nor any of its affiliates guarantee any rate of return or the return of capital invested.

This commentary material is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security.

All investments and investment strategies carry risks of loss, including the possible loss of all amounts invested, and nothing herein should be construed as a guarantee of any specific outcome or profit. While we have gathered information from sources we believe to be reliable, we cannot guarantee the accuracy or completeness of the information presented.

The information in this material is confidential and proprietary and may only be used by the intended user. Toroso, its affiliates, or any of their officers or employees are not liable for any losses arising from the use of this material or its contents. This material may not be reproduced, distributed, or published without prior written permission from Toroso. Distribution of this material may be restricted in certain jurisdictions. Anyone receiving this material should seek advice to determine whether there are any restrictions in their jurisdiction.